Agency loans are the most cost-effective option for financing investment properties, but they can be the most complex to secure. While obtaining one for your first investment property is relatively straightforward, acquiring additional properties becomes more challenging due to Fannie Mae's stringent guidelines. Our platform simplifies the process, offering clear guidance, easy application steps, and state-compliant financing solutions to help investors efficiently navigate rental property loans, vacation rental financing, and commercial real estate funding.

Lenders typically evaluate agency loans by considering an investor's overall cash flow. This includes both personal income from steady employment and net operating income from rental properties. However, these loans come with several challenges for investors:

Extensive documentation,including two years of complete tax returns with all accompanying schedules

A slow and uncertain approval process with high reserve requirements, which increase based on the number of properties you already have financed (the more mortgages you hold, the more liquid assets you must have).

Higher down payment Lenders typically evaluate agency loans by considering an investor's overall cash flow. This includes both personal income from steady employment and net operating income from rental properties. However, these loans come with several challenges for investors:

Restrictions Cash-out refinances and investment property loans are popular financing options for real estate investors.

The inability borrowing under a legal entity for real estate investments offers several advantages, including asset protection and anonymity. along with information on no income verification investor loans:

The need for a high enough income to maintain a solid debt-to-income (DTI) ratio. renovation loans, also known as rehab loans, allow investors to finance both the purchase and renovation of an investment property.

Why Regional Banks Struggle With No-Income Verification DSCR Loans: We Make It Simple. They Make It Hard. As a

real estate investor, you need fast, flexible financing that aligns with how you do business. DSCR (Debt Service

Coverage Ratio) loans offer an income-free path to funding based on property cash flow—not personal tax returns.

But try getting that from a regional bank, and you'll quickly hit roadblocks. We specialize in doing what

traditional banks can't—or won't.

The Challenges with Regional Banks

1. Outdated Lending Models

Most regional banks still rely on traditional underwriting, requiring full income documentation—even for DSCR loans. That means W-2s, tax returns, and personal financial statements, even if your property easily covers the debt.

2. Limited DSCR Products

Banks often label loans as "cash-flow based," but in reality, they come with hidden income requirements, stricter credit overlays, or low loan-to-value caps. That's not a true DSCR loan. We offer the real deal.

3. Slow, Bureaucratic Processes

Need to close fast? Good luck. Regional banks often take weeks to approve what should be a straightforward investment loan. We move at the speed of your deals, not theirs.

4. Low Appetite for Real-World Deals

Banks love perfect borrowers and perfect properties. If you're investing in transitional neighborhoods, short-term rentals, or scaling rapidly, they'll hesitate. We won't.

5. Inflexible Underwriting

A true DSCR loan is about the property—not your personal finances. Banks blend in DTI ratios and credit overlays that don't belong. We stick to what matters: property performance.

Why Investors Choose Us

- True No-Income Verification

No tax returns, no W-2s, no hassle

- Fast Approvals & Closings

15–40 year options, interest-only available, and more

- Investor-Friendly Mindset

We work with you—not against you.

Ready to Bypass the Bank and Get Funded?

We are built for real estate investors—not traditional borrowers. If you're tired of the delays, red tape, and rigid rules of regional banks, let's talk.

Apply today and get a DSCR loan that actually works the way it should.

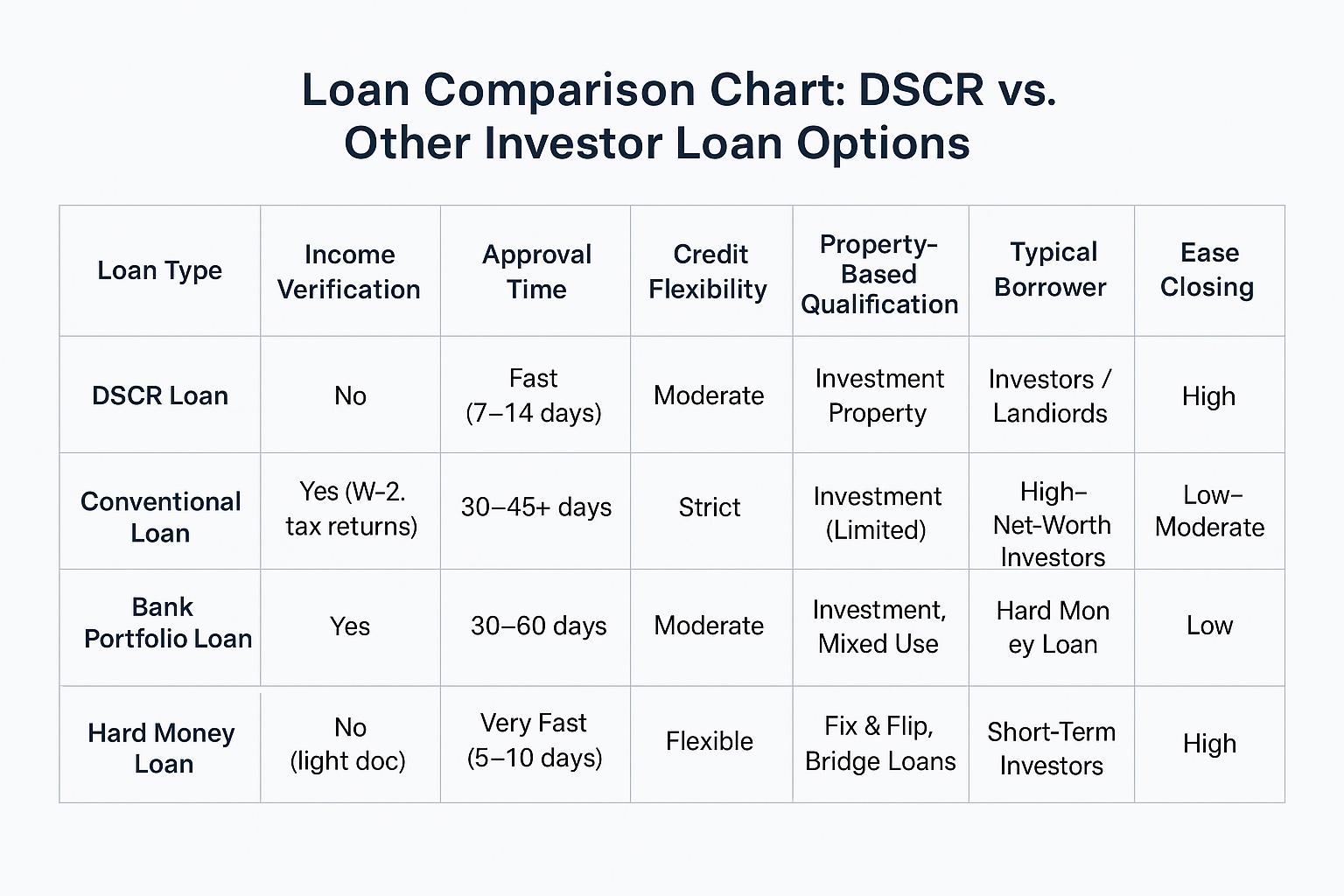

Loan Comparison Chart: DSCR vs. Other Investor Loan Options

Why DSCR Loans Are the Best Option for Investors

1. No Personal Income Needed

DSCR (Debt Service Coverage Ratio) loans qualify based on rental income—not your personal income. That means no W-2s, no tax returns, no personal DTI ratios. It’s the simplest, most direct path to funding for investors.

2. Faster Closings = More Opportunities

With approval timelines as fast as 7–14 days, DSCR loans help you move quickly and competitively in today’s fast-paced market. Conventional and bank loans can take 30–60 days or more, often costing you the deal.

3. Scale Your Portfolio Without Hitting Limits

Each DSCR loan is based on the income of the individual property—not your global DTI or income cap. This makes it easy to scale your investments property by property, with no personal income bottlenecks.

4. Flexible Credit Standards

While lenders do review credit, DSCR programs are far more forgiving than conventional or bank loans. Mid-600s credit scores can often qualify—especially with strong property cash flow.

5. Built for Real Estate Investors

Unlike conventional loans that were built for homebuyers, DSCR loans are designed for rental property investors. Whether you’re acquiring long-term rentals, short-term vacation properties, or small multifamily deals, DSCR is structured for cash flow and ROI, not owner-occupancy.

6. Chasing “Better Terms” Often Leads to Worse Outcomes

Yes, a bank or conventional lender might offer a slightly lower rate—but at what cost?

- Weeks of paperwork

- Risk of denial

- Slower closings

- Missed deals

The time, effort, and uncertainty can cost you more than any rate savings.

eDSCR Makes It Easy

We specialize in true no-income-verification DSCR loans that get investors funded faster, with less friction.

- No personal income verification

- Property-based underwriting

- Fast closings

- Scalable structure for long-term growth

Conventional Loan vs. Business-Purpose DSCR Loan: Understanding the Key Differences

When financing an investment property, choosing the right loan type is crucial. Two common options are conventional loans and business-purpose Debt Service Coverage Ratio (DSCR) loans. Each has distinct qualification criteria tailored to different investor needs.

🏠 Conventional Loan: Ideal for Owner-Occupants and Investors with Strong Personal Finances

Overview:

Conventional loans are traditional mortgages offered by banks and credit unions, typically conforming to guidelines set by Fannie Mae and Freddie Mac. They are suitable for primary residences, second homes, and investment properties.

Qualification Criteria:

- Income Verification: Requires proof of income through W-2s, tax returns, and employment history.

- Credit Score: Minimum of 620, though higher scores (640+) may be needed for better rates.

- Debt-to-Income (DTI) Ratio: Typically below 43%.

- Down Payment: As low as 3% for primary residences; higher for investment properties.

- Interest Rates: Generally lower, ranging from 5% to 7%.

- Loan Terms: Standard terms of 10, 15, or 30 years.

- Property Types: Single-family homes, condos, and multi-unit properties.

Pros:

- Lower interest rates and down payments.

- Widely available through various lenders.

- Regulated under federal mortgage guidelines, offering consumer protections.

Cons:

- Stricter income verification and credit score requirements.

- Longer approval process due to extensive documentation.

- Limited flexibility for investors with fluctuating income.

💼 Business-Purpose DSCR Loan: Tailored for Real Estate Investors

Overview:

DSCR loans are non-qualified mortgage (Non-QM) products designed for investors focusing on rental properties. These loans prioritize the property's income potential over the borrower's personal financial situation.

Qualification Criteria:

- Income Verification: Not required; approval is based on the property's rental income.

- Credit Score: Typically 620 or higher.

- Debt-to-Income (DTI) Ratio: Not considered.

- Down Payment: Generally 20% to 30%.

- Interest Rates: Higher than conventional loans, ranging from 6% to 9.5%.

- Loan Terms: Flexible terms, often 15 to 30 years.

- Property Types: Rental properties, including single-family homes, multi-family units, and short-term rentals.

Pros:

- No personal income verification required.

- Faster approval and closing processes.

- Allows for financing multiple properties without impacting personal credit.

- Suitable for self-employed individuals or those with inconsistent income.

Cons:

- Higher interest rates and down payment requirements.

- Not widely available through traditional lenders.

- May require a minimum DSCR (e.g., 1.0 or higher) to ensure the property generates sufficient income to cover the loan.

🔍 Comparison Overview

| Feature | Conventional Loan | Business-Purpose DSCR Loan |

|---|

| Income Verification | Required (W-2s, tax returns) | Not required |

| Credit Score | 620+ (higher scores preferred) | 620+ |

| DTI Ratio | Typically below 43% | Not considered |

| Down Payment | 3%–25% (varies by property type) | 20%–30% |

| Interest Rates | 5%–7% | 6%–9.5% |

| Approval Process | Longer, due to documentation | Faster, with less documentation |

| Loan Terms | 10, 15, or 30 years | 15 or 30 years |

| Property Types | Primary residences, second homes, investment properties | Rental properties, including short-term rentals |

✅ Which Loan Is Right for You?

- Choose a Conventional Loan: if you're purchasing a primary residence or second home and have a stable income and strong credit history.

- Opt for a Business-Purpose DSCR Loan: if you're an investor focusing on rental properties, especially if you have fluctuating income or wish to finance multiple properties without impacting your personal finances.

For personalized advice and to determine the best financing option for your investment goals, consult with a mortgage professional experienced in both conventional and DSCR loan products.